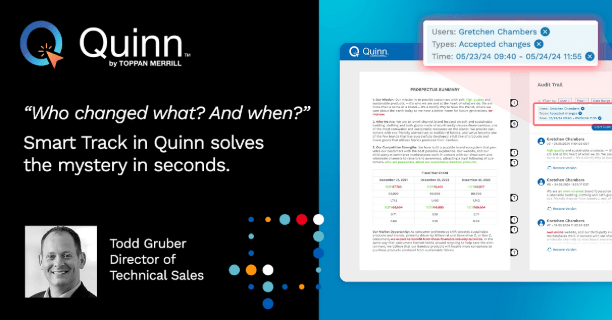

“Who changed what? And when?” Smart Track in Quinn solves the mystery in seconds.

Trying to pinpoint a single change in your proxy statement can quickly turn into a time-consuming exercise. Comparing document versions...

Todd Gruber - Director of Technical Sales